Today, I'm here to talk about the last export incentive that exists in our Internal Revenue Code. This incentive has been around since 1971 and was revamped in 1984. Due to the Bush tax legislation passed in the early 2000s, this regime became effective and a part of planning for many exporters. This particular incentive is known as the interest charged domestic international sales corporation, commonly referred to as an acronym IC-DISC. This regime allows exporters of produced goods or extracted goods in the US, such as agricultural products, minerals, and other resources, to have approximately 50% or half of their export income subject to a reduced effective tax rate. The IC-DISC is primarily geared towards helping small and mid-sized exporters, although publicly traded companies can also utilize it, but with diminished tax benefits. Therefore, before considering incorporating or including a DISC as part of their tax planning strategy, small and mid-sized exporters need to ask themselves a couple of questions. Firstly, they need to determine if their products are ultimately used outside the US or exported for use outside the US. Secondly, they need to assess their current export volume, as there are costs associated with setting up and administering the IC-DISC, and the benefits should outweigh these costs. Additionally, exporters should consider their net margin or profitability on their exports. If they are not profitable, the regime may not significantly benefit them. It is crucial to be profitable in order to take advantage of this incentive. Once exporters know the answers to these questions and their export volume is approximately a million dollars or greater, or the net export income is $200,000 or greater, there is likely an opportunity to implement the IC-DISC regime. It's important to note that the IC-DISC is invisible to your operations, meaning you do not have to change your...

Award-winning PDF software

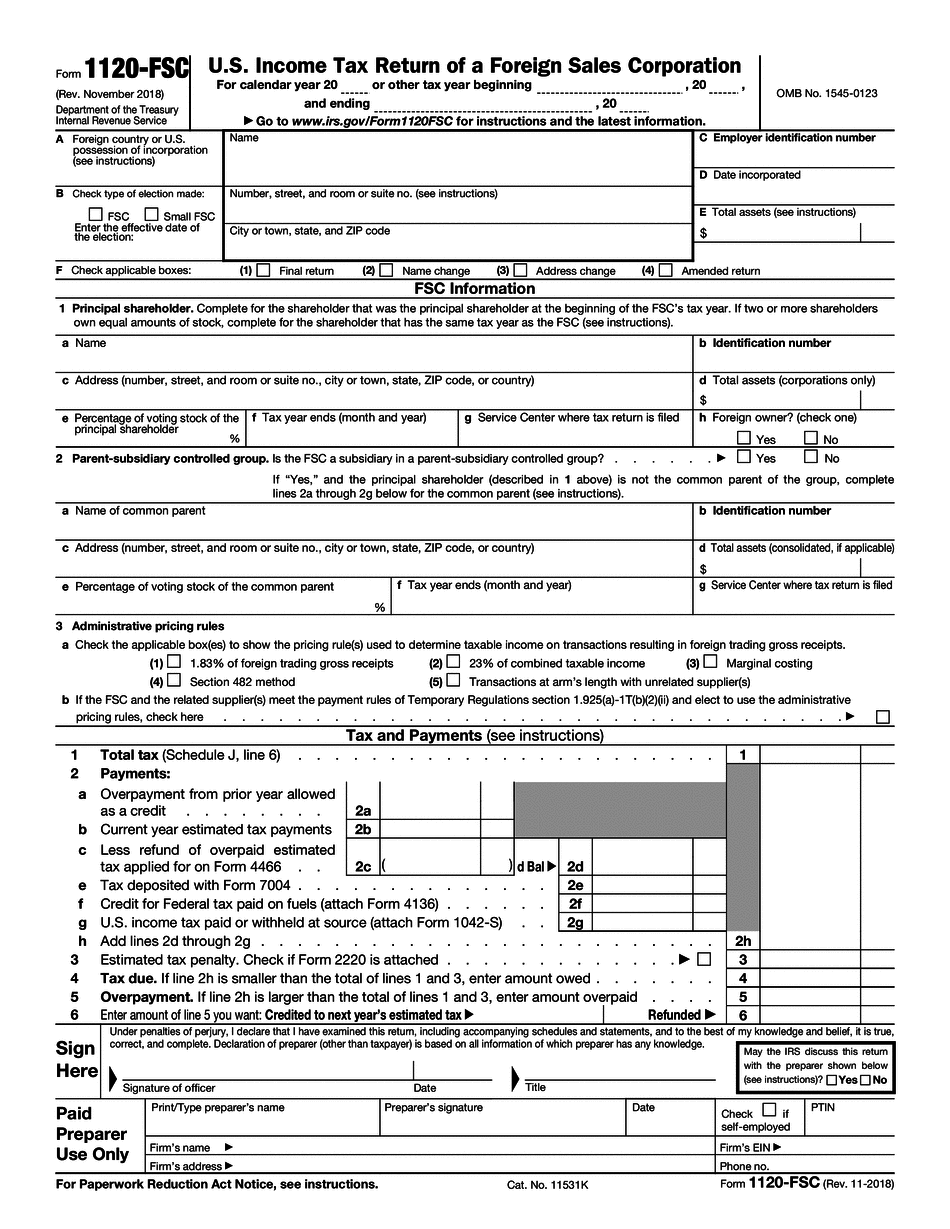

Domestic international sales corporation Form: What You Should Know

Of its total revenue from sources outside the United States and 99.9%... Domestic International Sales Corporation — Tax Guide This is a tax guide for domestic sales corporations. It describes what each income category is taxed, and explains the various tax options available to you if you have a domestic sale corporation. Interest Charge Domestic — United States This form (I-864) is used to report the tax on the tax charge for interest expense. Domestic Sales Corporation Interest Charge Income — IRS For the purpose of interest cost as stated in IRC 6166. The deduction for interest expense can be taken on Form 1120-I or Form 1120-C. You can use either Form 1120-I or Form 1120-C if you meet the rules. Form 1120-I can be completed by your own bank with all information correct. Form 1120-C is also a reasonable method if your bank accepts Form 1099 for interest expense; even then, there are rules that govern the method. You can report as income and pay tax on a Form 1120-I or Form 1120-C. However, depending on your situation or your bank's acceptance of forms, you may have to complete and send Form 1099 (or other acceptable form) for form 1120-I or Form 1120-C if you use that method. If interest is paid to the trust, the trust corporation, in turn, reports interest expense as the trust income. Interest expense may or may not be included in the deduction if the trust corporation is not a domestic corporation. Interest Charge Domestic — Foreign Country This form (I-831) is used to report the tax on the tax charge for interest expense. Interest Charge Domestic — United States This form (I-864) is used to report the tax on the tax charge for interest expense in the United States. It is useful for domestic corporation because U.S. tax law allows deduction for interest expense with a single deduction for foreign profits. However, if you are selling or transferring goods or services outside the United States you still need a foreign country tax payment. The foreign country tax payment will be shown on your Form 1120-C under the country code for the sales or service. Interest Charge Domestic MUST — IRS This is an information return (Form 1120-I) that is used to report interest income on a Form 1120-T.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 1120-FSC, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 1120-FSC online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 1120-FSC by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 1120-FSC from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Domestic international sales corporation